Stablecoin has undoubtedly become the hype of 2018 with its 700%+ annual growth. A lot of discussions arise around this hot topic, and most people believe stablecoin is suspicious with problems such as lack of transparency and high centralization/single-point failure.

As of today, three stablecoin mechanism designs have been invented. To most people, none of the three stablecoin mechanism designs is good. However, regardless of many flaws, Basis Protocol (previously Basecoin), one stablecoin, has attracted $133 million from a list of big-name VCs: Lightspeed Venture, Google Ventures, Bain Capital Ventures, and Andreessen Horowitz.

In this article, I am not going to repeat much about the stablecoin 101. Instead, I will primarily focus on analyzing the non-collateralized/growth-backed type stablecoins using Basis Protocol as an example.

Summary

- The best result for the fiat-collateralized stablecoin is that governments/banks/highly regulated entities will issue the coins with their reserve. These coins are just digital versions of the existing currencies with the same limits.

- The crypto-collateralized stablecoin mechanism will not work since it may still have a high volatility.

- The non-collateralized/growth-backed stablecoins (‘Seigniorage Shares’) may work in the short term before the demand stops growing. However, it may not work in the long run since there is not a permanently growing demand.

- Though the growth-backed stablecoins, such as Basis Protocol, are not a good idea, they can be good investment opportunities. The TAM for Basis can be as huge as $108.901 billion.

- The growth-backed stablecoins are printing free money that will eventually depreciate when the growth ends. This mechanism can become a Ponzi scheme if the growth cannot be sustained.

Background

If you have the basic knowledge of stablecoins, you can skip this section.

Due to the high volatility, cryptocurrencies have never been widely used as an exchange medium since their existence. No merchant will want to accept a coin that values $100 at this moment while only $50 in the next hour. To address this volatility issue, people invented the Stablecoins, which are price-stable cryptocurrencies.

To achieve the stability, three types of stablecoins have been introduced:

- Fiat-collateralized stablecoins

- Crypto-collateralized stablecoins

- Non-collateralized stablecoins (‘Seigniorage Shares’-type/Growth-backed stablecoins)

1. Fiat-collateralized stablecoins are the coins backed by fiat (e.g. USD) reserves. The most prominent example is Tether, which dominates the major stablecoin market now. For the Fiat-collateralized stablecoins, the major challenges are:

(1) Highly centralized — the currency is backed by one company

(2) Lack of transparency — it is difficult to verify the reserve

(3) Lack of scalability — it is difficult to scale up with a 1:1 reserve

(4) Difficulties in bank relationships — it is highly possible that government will intervene and banks are highly regulated

Long Story Short:

(1) Tether has not been audited yet, and a lot of research (source 1, source 2) indicate that they may just be a Ponzi scheme;

(2) New audited USD-pegged cryptocurrencies such as Paxos are being issued, while they will be regulated by local government.

Conclusion: the best scenario for this stablecoin design is that governments and/or banks will issue these stablecoins with their reserves. It will just be a digital version of the existing currencies, which will not be freely used worldwide.

2. Crypto-collateralized stablecoins are stablecoins that are backed by other cryptocurrencies such as Bitcoin and Ethereum. To provide sufficient stability, these stablecoins will prepare excessive reserve. For example, to issue 100 stablecoins, each of which values $1, an issuer will reserve some Bitcoins or Ethereums that value $200. However, what would happen if the price of the coins used as reserve drops dramatically and the issuer cannot provide more reserve?

Conclusion: this is simply a bad idea since the value of other coins are highly volatile (and correlated) and a high reserve rate will never provide sufficient stability.

3. Non-collateralized stablecoins (‘Seigniorage Shares’-type/Growth-backed stablecoins) are stablecoins that are not backed by any real/digital asset. Instead, the issuer use an algorithm to control the supply/demand of the stablecoins to stabilize the price (e.g. at $1 per coin). I will elaborate on this type of stablecoins in the next section.

Basis Protocol: a growth-backed stablecoin

1. Mechanism

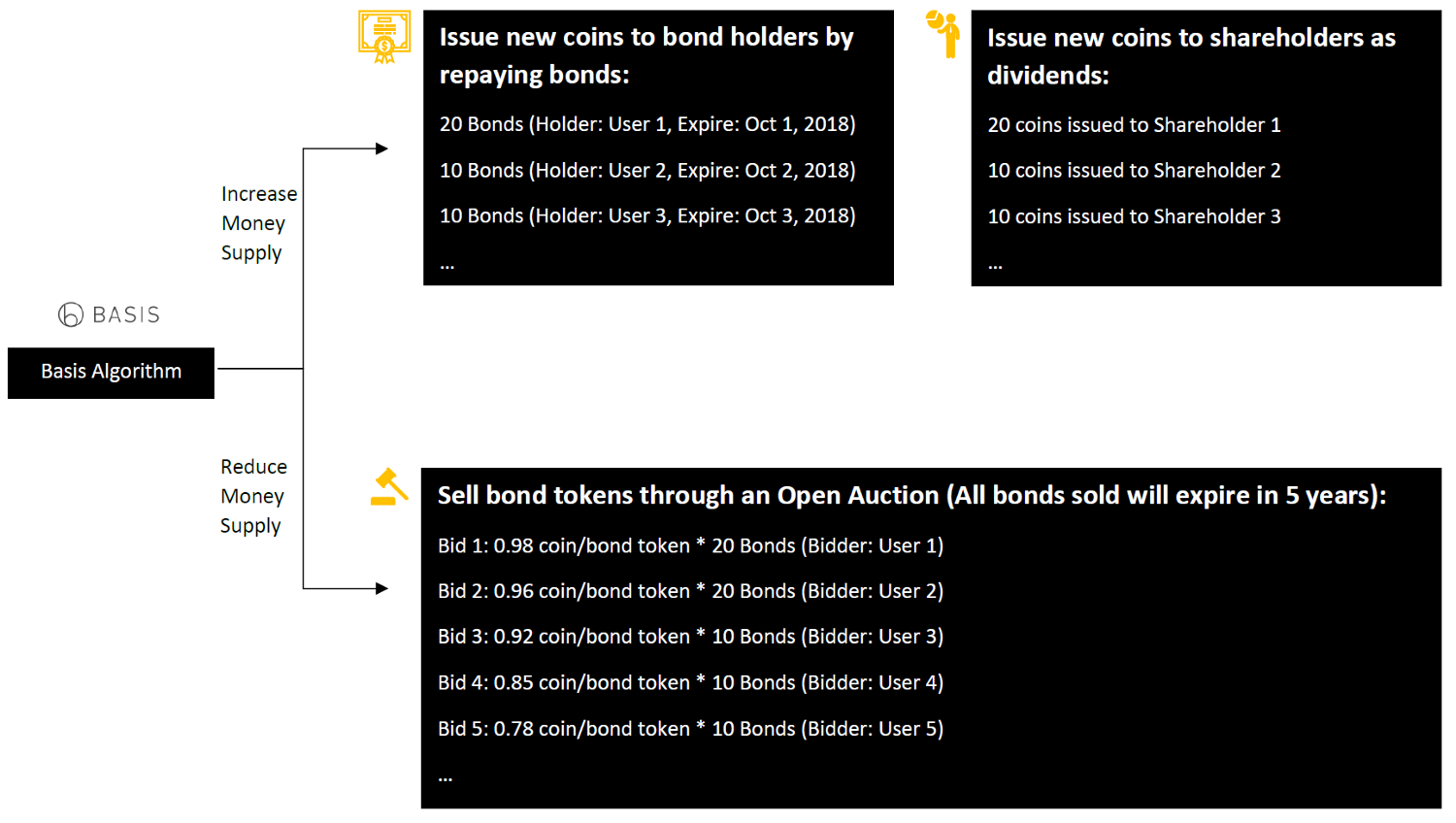

The Basis protocol has three different tokens — ‘Basis’ (the stablecoin), ‘bond tokens’, and ‘share tokens’. The mechanism of this protocol is much like that of the central banks: when the price of Basis goes over $1, the Company (Intangible Labs) issues more Basis; when the price of Basis goes below $1, the company sells bond tokens with 1-Basis face value for less than 1 Basis to reduce the Basis supply in circulation.

Expansion (Increase money supply)

When the price of Basis goes over $1, the Company will increase money supply by issuing new Basis through bondholders and share token holders.

Bondholders are paid first, and in first-in-first-out (FIFO) order. If there are any outstanding bond tokens, the blockchain begins converting bonds into coins, one-for-one, according to their order in the Bond Queue (the oldest bond first).

Shareholders are paid after bondholders. If there are no more outstanding bond tokens, the system distributes any remaining new coins to shareholders as a dividend.

Contraction (Reduce money supply)

When the price of Basis goes below $1, the Company sells bond tokens through an open auction system.

In order to sell bonds, the blockchain runs a continuous auction in which bidders specify a bid and bid size for new bond tokens. In other words, auction participants specify how much Basis they want to pay for each bond and how many bond tokens they want to buy at that price. For example, one can specify that they would like to purchase 100 bonds for 0.9 Basis per bond. When the blockchain decides to contract coin supply, it chooses the orders with the highest bids and converts the holders’ coins into bonds until sufficient Basis has been destroyed.

2. How the system will work

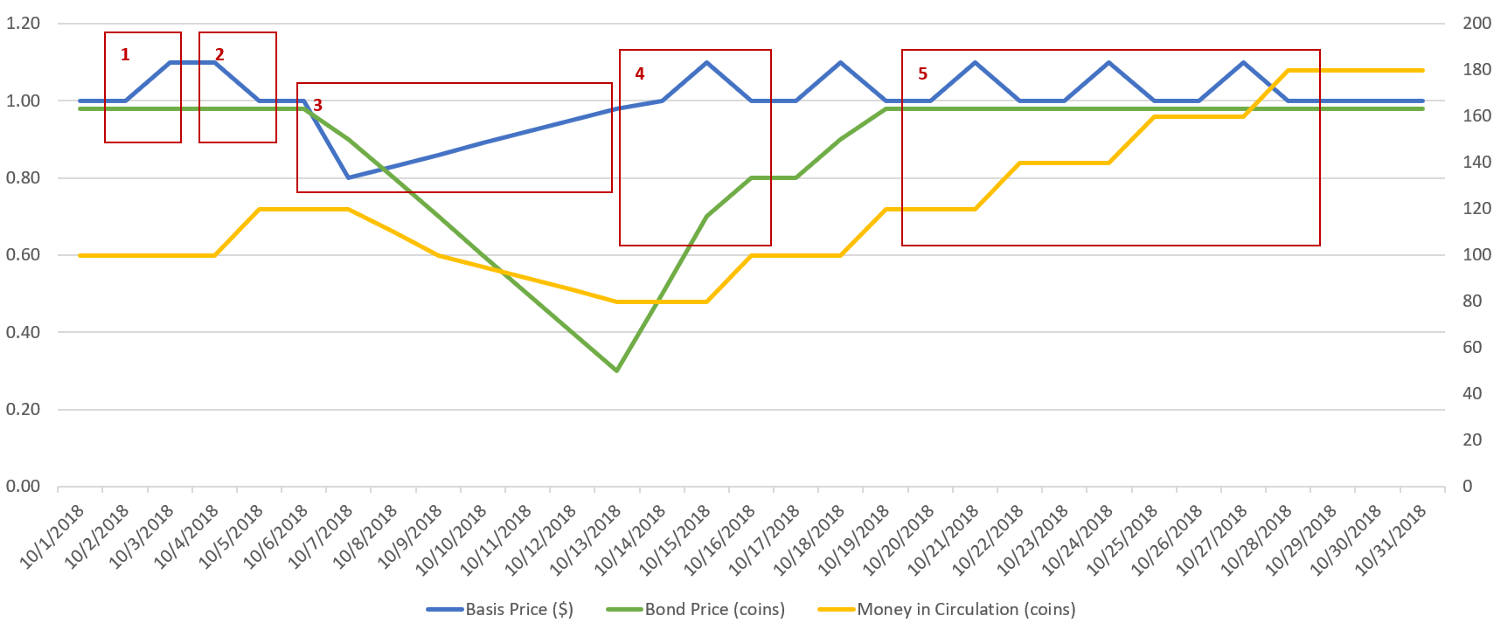

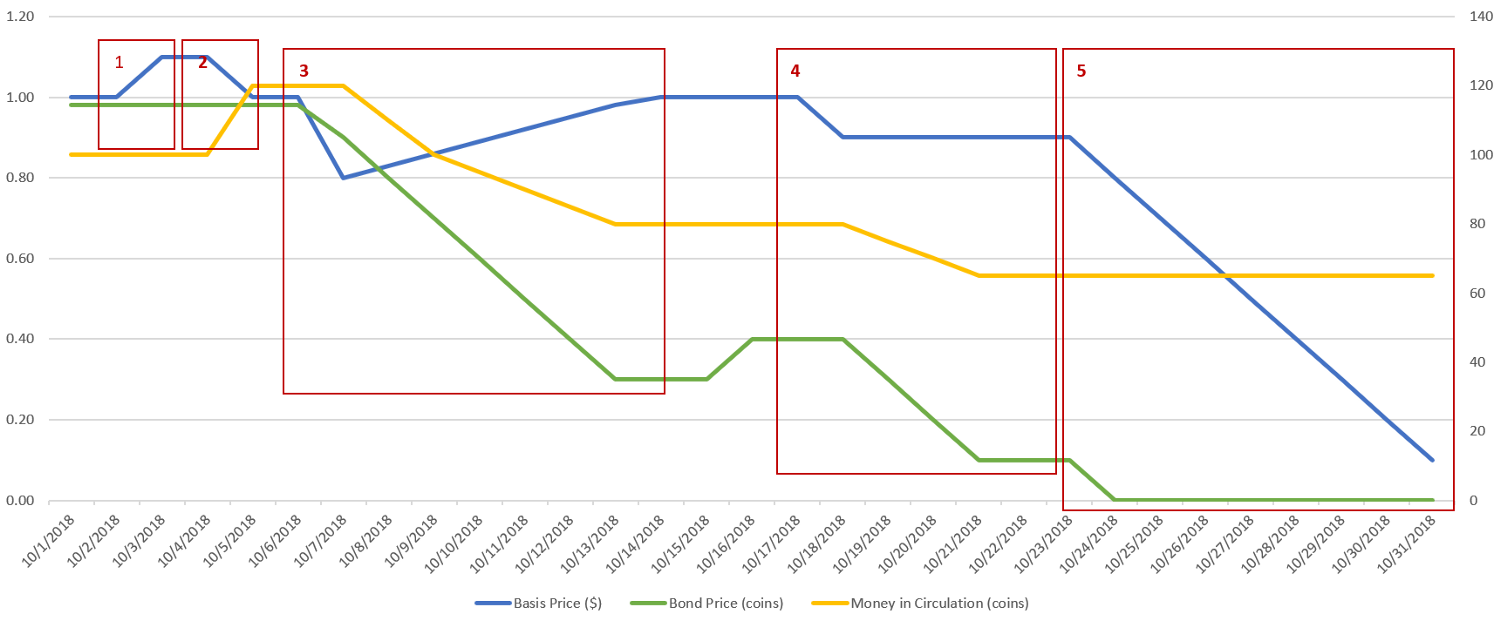

The Basis Protocol is expected to work as shown in the diagram:

We assume we already have 100 coins, each of which values $1, in circulation. We also assume there is a secondary bond market where the bond token with 1-coin face value is sold at a price slightly lower than its face value (e.g. 0.98 coin/bond token) if people believe the bond can be paid soon in the future.

At stage 1, there is a new demand of 20 Basis (e.g. from people who lose confidence in Turkish Lira. More sources of new demand will be discussed in the following section). The price of Basis therefore rises to $1.10 per coin. To bring the price back to $1.00 per Basis, the algorithm calculates how much new supply is needed and then issues the new Basis through repaying old bond tokens and paying dividends to shareholders.

At stage 2, the price of Basis goes down due to the new supply.

At stage 3, the demand decreases by 40 (e.g. many people sell the Basis for USD to hold back Turkish Lira or buy other assets.). The algorithm starts to sell bonds to people who provides the highest bidding price in the open auction system. After fulfilling all the bids of 0.98 coin per bond, the algorithm starts selling the bond-token at 0.9 coin per bond, 0.8 coin per bond, 0.7 coin per bond… until it collects and burns enough coins to reduce the supply and recover the Basis price to $1.00 per coin.

The longer it takes the algorithm to recover the price, the lower the bond token price will be, and the longer people will suffer from the temporary low Basis price.

At stage 4, new demand comes soon after the decrease. The oldest bond tokens are paid at its face value (1 coin/bond token), and people gain confidence about the bond tokens in the future.

At stage 5, as long as there is constant new demand, people will be confident about the bond tokens, and the bond token will recover its price to the normal level, which is slightly less than its face value, just like the normal treasury bond.

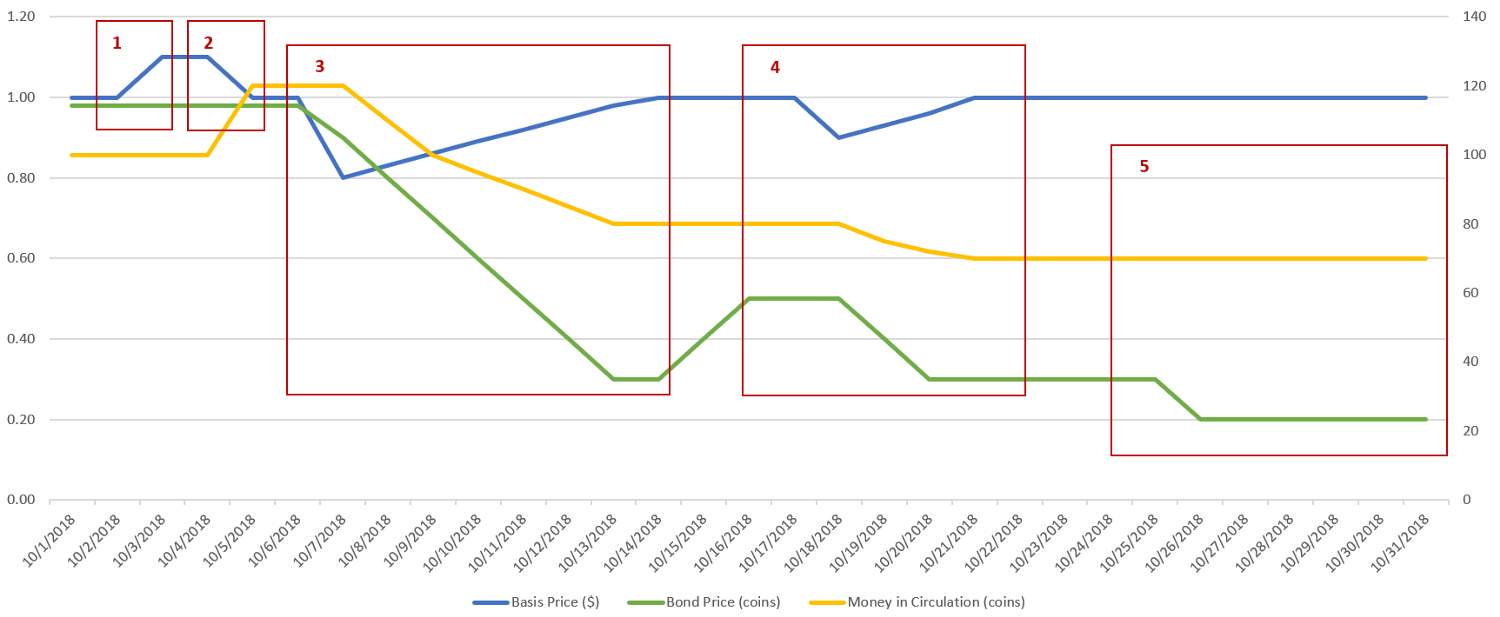

3. How the system will really work

However, a different story can be told within the same mechanism:

At stage 1, stage 2, and stage 3, what the algorithm will do is the same as in the last scenario.

At stage 4, however, Basis Protocol gets a lower demand (e.g. people are dealing well with their fiat/a low growth of cross-border transactions/better exchange medium invented). The bond token price will go down again since the old bond tokens have not been paid out, and there is a higher risk that the new tokens will never be paid.

At stage 5, the longer time before Basis receives a new demand, the lower the bond token price, and the more difficult for Basis to recover the $1/coin price next time.

A worse but more possible story would look like this:

At stage 1 and stage 2 what the algorithm will do is the same as in the last scenario.

At stage 3, it takes a long time for Basis to recover the price since people do not have sufficient confidence about its future and do not buy the bond tokens. Therefore, the bond token price goes to very low.

At stage 4, instead of seeing a growing demand, Basis receives a decreasing demand. However, since the bond price is already very low — people do not want to buy because a lot of old bonds have not been paid — the algorithm is unable to recover the Basis price for a long time.

At stage 5, people start to sell Basis because they cannot expect the price to recover and have the fear of that Basis price will keep going down.Both the price of Basis coin and the price of Basis bond token drop quickly to zero.

4. What the problems are

According to the above analysis, two major problems exist in the mechanism:

(1) A continuously growing demand is required to maintain the price of bond tokens, which will be used to maintain the price of Basis coins. The price of Basis bond tokens relates to people’s confidence about Basis’s future growth, since bondholders can only gain profit when new coins are issued and old bonds are paid.

The Basis team has set a price floor and 5-year expiration for bond token to avoid its price going too low. However, setting a price floor will not solve the problem since there can be a secondary market that values the bonds lower than the floor. Having a 5-year expiration will also not help since it is possible that the bonds will still not be paid at expiration.

(2) It is possible that the Basis coin will be undervalued for a long time.As shown in the Stage 3 of the last two scenarios, it is possible that the algorithm cannot recover the Basis price quickly. In that case, the stablecoin is no longer “stable” since its value is lower than what it claimed ($1) for a long time.

5. Why it is a bad idea

As discussed above, the success of such a central bank system will require (1) a continuously demand growth (2) the ability to increase/reduce money supply quickly.

Basis cannot expect a continuously growing demand. Eventually, Basis will not replace fiat (e.g. Basis could not be used for paying tax), and the demand of Basis will not be affected by factors such as GDP. Instead, the demand of Basis will be affected by:

(1) The performance of fiats (e.g. people will convert Turkish liar or Venezuelan bolívar to Basis to avoid depreciation);

(2) The volume of cross-border remittances (we assume using Basis can reduce the cross-border transaction cost);

(3) The volume of cryptocurrency transactions (we assume people will still not use fiat for cryptocurrency exchange in the future).

Basis does not have many tools to cut money supply. Basis can only cut the supply by selling bonds or by purchasing the coins with its own reserve. However, governments/central banks can leverage a series of other tools: (1) increase reserve rate; (2) increase interest rates (though Basis can increase “interest rates” through lowering the bond price, this “interest” is not guaranteed since the bonds can expire without being paid) ; (3) decrease discount rate; (4) decrease government spending, and (5) increase taxes.

6. Why it can be a good investment

From an investor’s perspective, regardless of the flawed mechanism design, Basis can still be a good investment opportunity.

As mentioned above, the growth of the demand of Basis will primarily come from three sources: (1) the performance of fiats; (2) the volume of cross-border remittances; (3) the volume of cryptocurrency transactions.

We can do some rough calculations here.

(1) Demand from people holding “bad fiats”

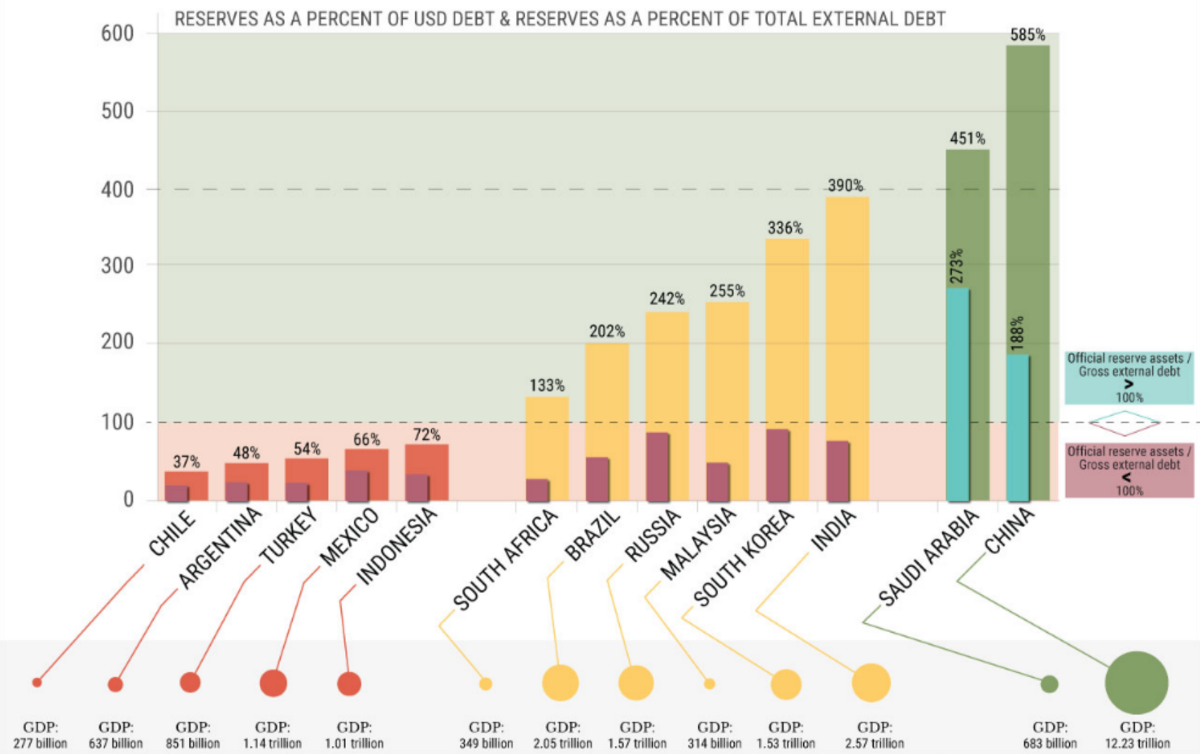

According to Geopolitical Futures, several countries are experiencing currency crisis since their reserve cannot cover their external debts. In these countries, local currencies depreciate dramatically, and therefore the currency holders have the incentives to convert the fiat to Basis.

For these countries, we estimate the demand using the following model: M2 of bad-fiats * Conversion Rate. (M2 Data source: CEIC Data)

(2) Demand from cross-border remittances

The world remittance data can be found on the World Bank Group website. With this data, we estimate the demand using the following model: World Remittance volume * Conversion Rate.

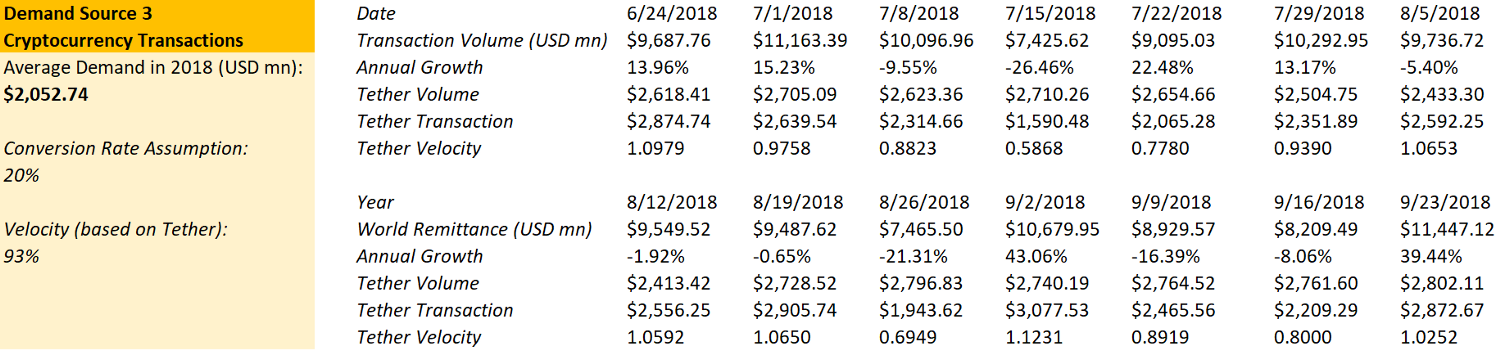

(3) Demand from cryptocurrency transactions

With the Fisher Exchange Equation (MV = PT), we can estimate the demand using the following model: Transaction Volume * Conversion Rate / Velocity.

Under our conversion rate assumptions, we can estimate the TAM (total addressable market) of this Basis Protocol to be (100,688.34 + 6,160.00 + 2,052.74) = $108,901.08 (USD mn) = $108.901 billion USD.

Different from the TAM for services/products, this TAM will not replicate from year to year. Moreover, this TAM will possibly shrink if there is fewer bad fiats, fewer remittances, or fewer cryptocurrency transactions.

However, regardless of the potential shrinking, the TAM is extremely attractive to any investor, not to mention that there is nearly no cost at all.When new demand of Basis comes, the algorithm will just “print” money and issue to the investors — if investors believe it is far from the end of growth, they will take all the new coins by buying bond tokens and/or receiving dividends from their share tokens.

That being said, before it comes to the end of growth, about $108.901 billion free money is going to be issued to investors (without discounting to present value or considering the demand growth). The investors will then sell the coins to people from the three demand sources at $1 each. The only thing that all investors need to do is to convert all their Basis coin inventory back to USD before the end of growth.

Undoubtedly, it is a good investment opportunity, given the money Basis raised ($153M) and its potential return. However, is this eventually a new Ponzi scheme? A ticking time bomb? We’ll see.

This research project is completed through a collaboration between Fan Wen at Yale SOM and Josh Liggett at OurCrowd.

Disclaimer: The article is not, and should not be regarded as “investment advice” or as a “recommendation” regarding a course of action, including without limitation as those terms are used in any applicable law or regulation.