Yesterday, I was reading an article shared by Kai from Sequoia China on the latest trends of consumer behaviors as well as the B2C investment opportunities.

One thing that resonates with me a lot is that: retailers are getting closer and closer to the consumers — to steal market share from large supermarkets by offering services that are more convenient and much faster, and to grow the market size by attracting consumers to purchase more. Eventually, getting closer to consumers also means knowing consumers better with more data and selling more types of products and services to the consumers.

Interestingly, we observed the same trend in many other countries — from developed markets such as the US to emerging markets such as Brazil — with many startups working on the community-level “nano warehouse/distribution center/dark store” concept.

1. What is this?

There are many types of community-level stores. Here, we are talking about the latest type of store that usually covers population living within a range of 1 to 5 KM, has a footprint of 50 to 200 SQM, and also offers last-mile (usually 2H or same-day) delivery or 24H self pick-up service.

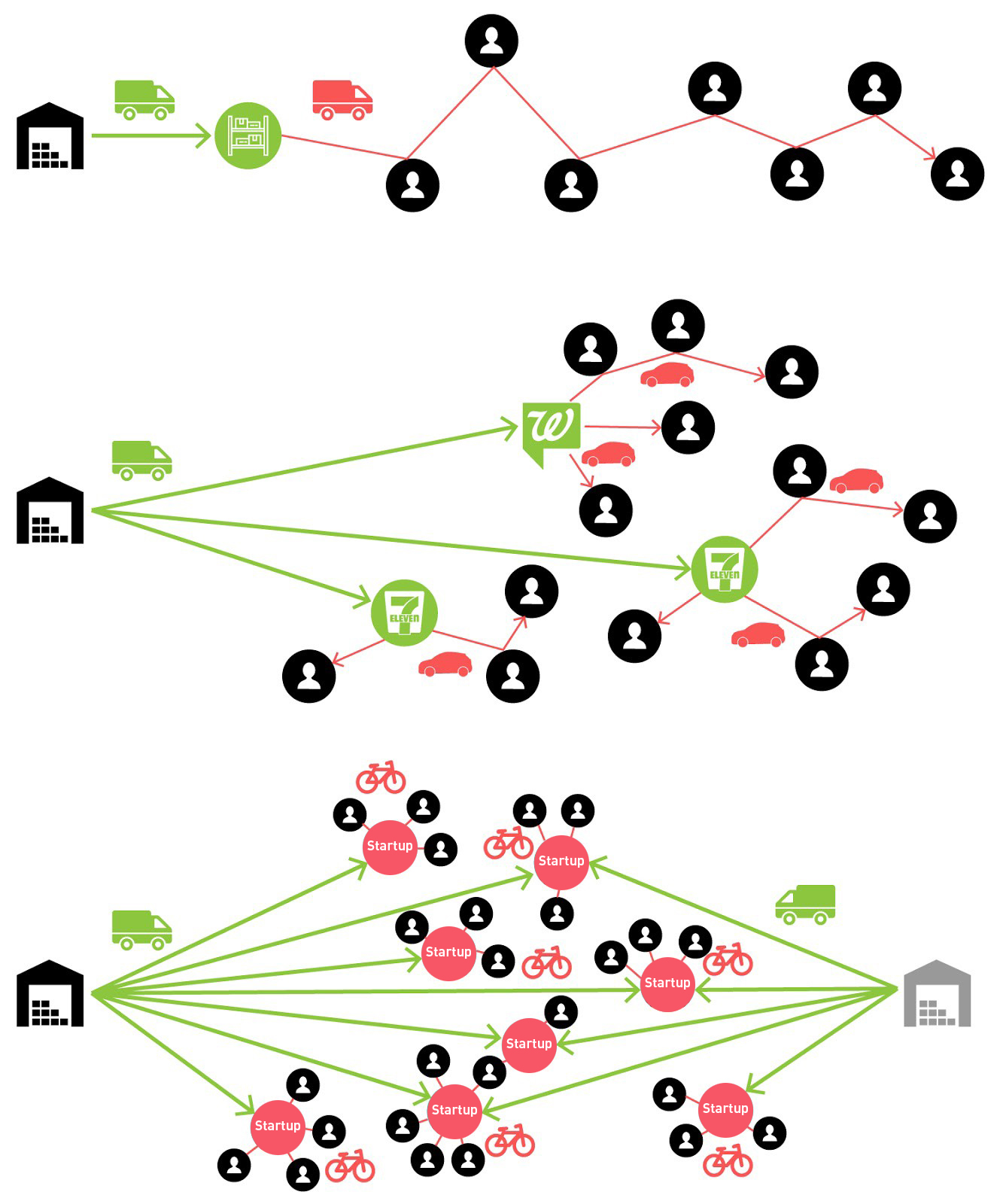

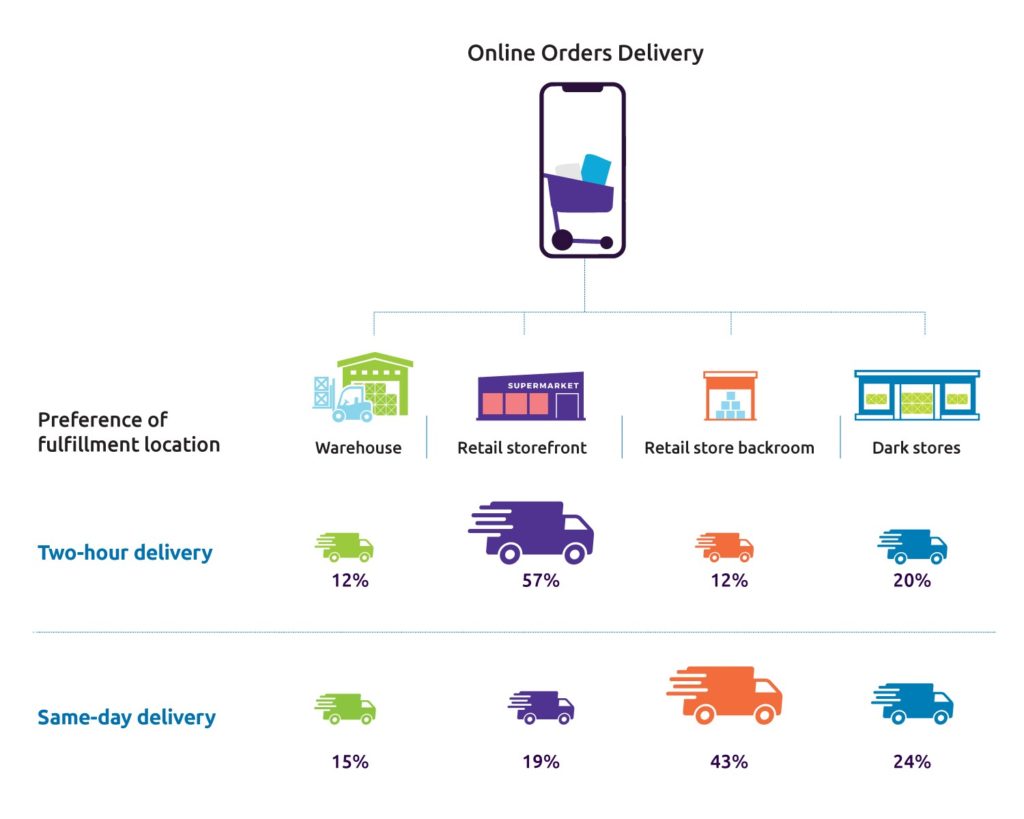

We can easily see the differences among the three logistics models: (1) Backend warehouse model: from regional warehouse to consumers (e.g. Amazon, traditional e-commerce); (2) Hybrid model: from regional warehouse to city-level distribution centers to consumers; (3) Front warehouse model: from regional warehouse to community-level nano distribution centers to consumers.

2. What has enabled this?

Apparently, this concept is not a rocket-science that’s invented just recently. To me, it is the rich consumer data and the increasing analytics/prediction capabilities brought by AI/ML that enable retailers to move closer to consumers.

With more consumer data and accurate ML-based purchasing prediction models, each store can precisely (hopefully) predict (1) what the nearby consumers want, (2) how much they want to buy, and (3) when they want to buy and deliver.

Therefore, with a more accurate prediction than before, retailers can open stores with a high number of SKUs and small inventories but still maintain a low operating cost.

3. What are the benefits?

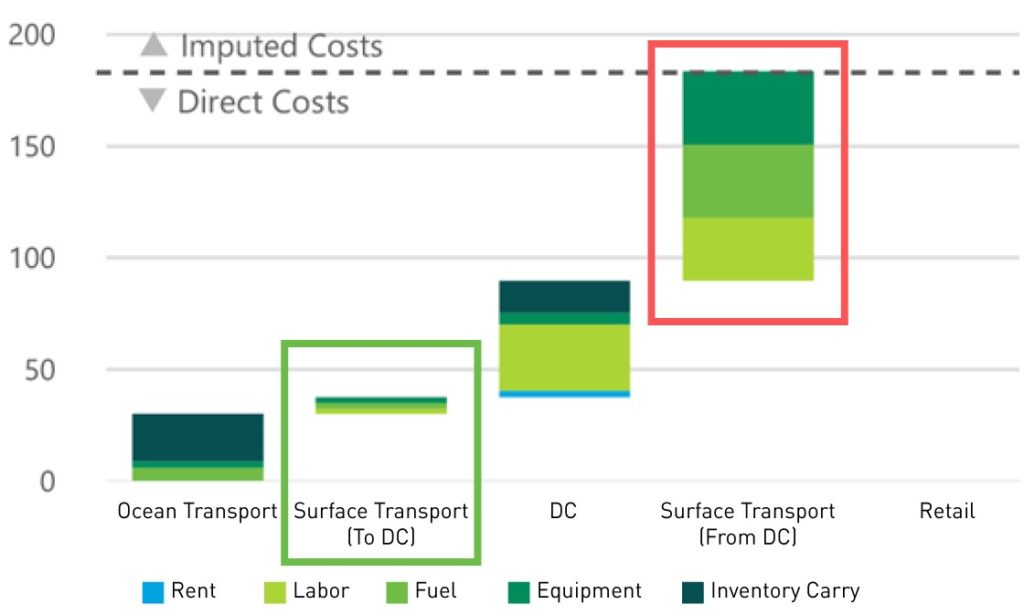

3.1 Lower last-mile and overall delivery cost

As a share of the total cost of shipping, last mile delivery costs are substantial — comprising 53% overall (Source). The reasons are fairly simple. First, inefficiencies from the local traffic. Second, inefficiencies from the inaccessibility of buildings/communities. Third, inefficiencies from scheduling and route planning/optimization — deliveries could only be done during the day time.

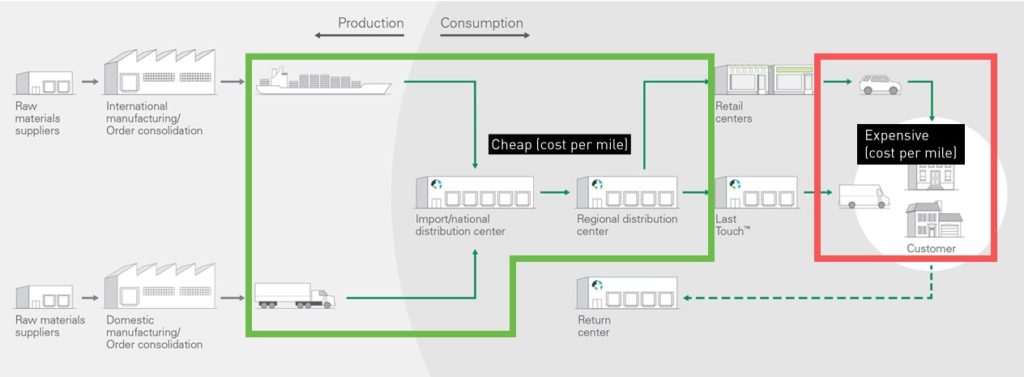

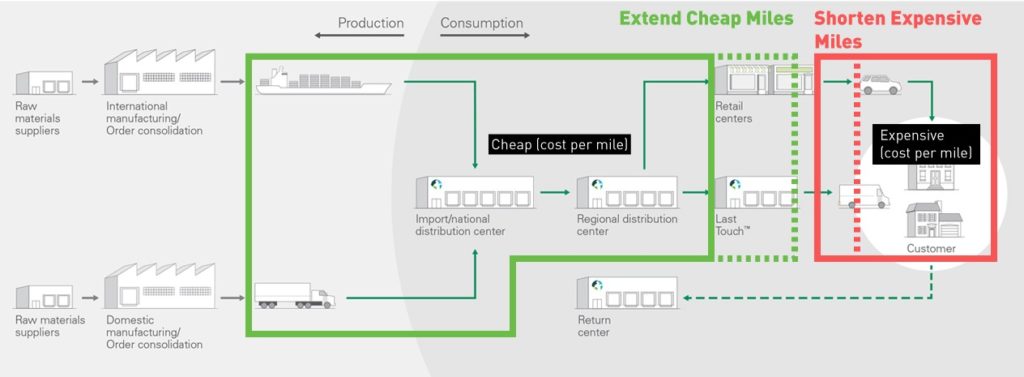

By shortening the last-mile delivery distance, retailers can dramatically reduce the overall delivery cost and increase the delivery speed as well.

The following diagram shows how it will work after retailers move the warehouses closer to the consumers.

3.2 Faster last-mile delivery

Apparently, with a shorter last-lime distance, retailers can shorten the delivery time as well. This is not something good to have, but it is a MUST for the next-gen consumers.

3.3 Higher frequency of purchase

Previously, consumers usually visit shopping centers or big super markets once per week, and they visit the convenience stores such as 7–11 probably three to five times per week.

When stores, particularly stores with Whole-Foods-level fresh food, are just near their places, consumers will be incentivized to purchase more for sure.

3.4 Higher diversity of goods that consumers can purchase at the door

As we mentioned in the second section, with a more sophisticated AI/ML- based prediction model, retailers can precisely predict what and how many products that consumers need. Therefore, they can increase the number of SKUs without increasing the waste.

On the other hand, this last-mile warehouse & delivery network will also enable the growing D2C brands to reach a much larger audience. Previously, opening local stores for a small D2C brand does not make economic sense, while the high logistics cost from the traditional models will limit the presence of these D2C brands.

4. How is it different from 7–11?

People might still be a bit confused about how this community-level “nano warehouse/distribution center/dark store” differs from the traditional convenience stores such as 7–11.

First, 7–11s usually do not provide delivery.

Second, the new stores can have higher number of SKUs than 7–11s. See the last section for the reasons.

Third, the new stores will have a much lower labor cost. Usually, these new stores will focus on delivery and self-pickup instead of having staff selling at the store.

Fourth, the new stores will have a lower per-SQFT operating cost. Since these new stores are more like warehouses, they do not need large passage spaces or nice shelves. Therefore, they can have a much lower per-SQFT operating cost.

Fifth, the new stores will have lower rent expenses. Since the new stores will operate more like a warehouse, they do not need to locate in the most crowded spaces. Instead, they can rent places that are a bit far from the main street (but still very close to the consumers) and therefore lower their rent expenses.

5. What is the bigger story?

For the Chinese investors, they always enjoy finding the “traffic entrance”. In the early stage, the traffic entrance are search engines such as Google and portal websites such as Yahoo. Today, Google is still one of the major entrances, but other entrances also emerge —such as Twitter/Facebook, Taobao/Amazon, and Weibo/Douyin.

Securing the traffic entrance means you can get more data about the consumers — knowing where they go, what they read/watch, what they purchase/plan to purchase, etc. Therefore, a traffic entrance is more than a single business.

In the digital space, it might take some time to find the next “traffic entrance” since people’s online-time has already been captured by the dominants.

In the physical space, however, it is still super fragmented. There is still a very high chance to find the next “traffic entrance” — it can be the “nano warehouse network”, the AV ride-sharing platforms (the ride-sharing market landscape is to be changed when autonomous driving is eventually coming), or something else.

—

This research is completed by Fan Wen with the help from Tarek Elessawi, Janis Skriveris, Marc Bouchet, and Addison Huneycutt at Plug and Play Ventures.

Disclaimer: The article is not, and should not be regarded as “investment advice” or as a “recommendation” regarding a course of action, including without limitation as those terms are used in any applicable law or regulation.