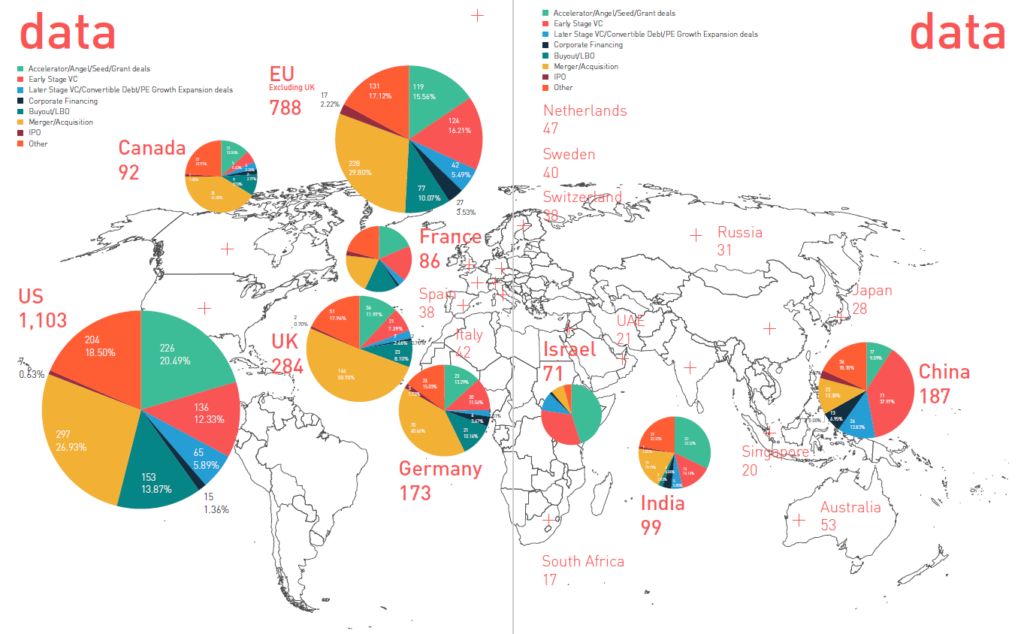

Some key findings are listed below. A full report can be found here: https://drive.wen.fan/Automotive-Mobility-Investment-2017-2018.pdf.

1. Investors are taking fewer risks, and it is more difficult to exit.

This is the overall investment trend in the automotive & mobility industry in 2018. Investors are becoming very careful when investing in early-stage companies, while investors will still write a big check if a company proves its value. For the later-stage companies in this industry, investors poured more capital to help companies develop products (e.g. L4 autonomous driving systems) and expand to increase market share (e.g. Didi Chuxing). However, with a significant drop in buyout/LBO, M&A, and IPO deals and a big increase in the “price”, it is more and more difficult for investors to find the buyers to exit.

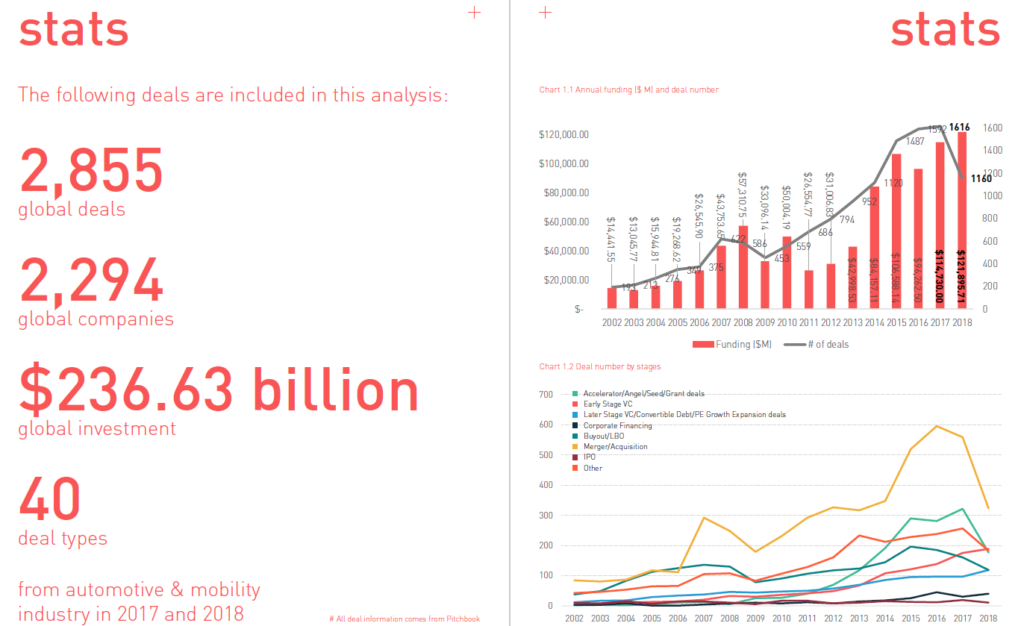

The deal size is getting much larger. The total funding increased slightly from $114.73 billion in 2017 to $121.90 billion in 2018. However, the number of deals dropped about 1/3 from 1,616 to 1,160. The average deal size, therefore, increased dramatically from $157.81 million to $214.98 million. This growth comes primarily from the super-early-stage companies that raised accelerator/angel/seed/grant fundings and the established companies that received later-stage VC/corporate fundings.

Accelerator/angel/seed/grant funding gets doubled in 2018. In 2018, there was about $1.05 billion invested in super-early-stage companies, while there was only about $0.54 billion in 2017. Notably, the number of deals decreased about half from 321 deals in 2017 to 177 deals in 2018, resulting in a much higher average deal size of $8.78 million ($2.56 million in 2017).

There were fewer exits, and the M&A deal size almost doubled. The number of buyout/LBO deals dropped about 25% from 160 in 2017 to 119 in 2018, the number of M&A deals fell nearly 43% from 559 in 2017 to 323 in 2018, and the number of IPOs also fell nearly half from 19 in 2017 to 11 in 2018. With the average M&A deal size almost doubled from $261.35 million to $491.50 million, it is reasonable to believe it is more difficult to find buyers for the established companies.

2. Autonomous driving developers need much more funding, autonomous truck becomes the hype, and there is little room for new entrants.

Six times more capital was invested into autonomous driving developers in 2018 ($7.82 billion) than in 2017 ($1.17 billion). About half of the funding was spent on later-stage VC deals ($3.39 billion), and the average deal size grew dramatically from $48.14 million to $1.69 billion. On the other hand, the accelerator/angel/seed stage deals dropped half from 33 deals to 18 deals with a similar deal size. This trend indicates that there is little room for new entrants, while more funding will be needed to support the late-stage companies to develop a practical product.

3. Perception is the key domain that attracts the most embedded software/hardware developers, and no one dominates yet.

Among the 85 deals for embedded software developers, 36 deals were closed for companies working on perception in 2017 and 2018. Following that, 17 deals were completed by companies working on mapping, and 14 for companies working on localization. Most of the perception solution developers are still in its early stage. 31 of the 36 deals from the past two years were early-stage deals (seed/angel/accelerator/grant/early-stage VC) with a total funding of $172.80 million and an average deal size of $8.85 million. For the embedded hardware developers, 39 out of the 50 deals were closed for companies working on sensors that help to improve perception with 28 deals closed for companies developing LiDAR. The LiDAR developers have raised $712.72 million in funding, and the average deal size for LiDAR developers was about $40.71 million in 2018.

4. The battle among transportation service platforms has not ended yet.

This segment has attracted the most significant portion (28.39%, $34.61 billion) of the total funding into the industry. Though the market has already been dominated by some large players such as Uber, Lyft, Didi Chuxing, Hertz, Avis, two times more funding has been invested in this segment. The established companies raised funding to get more market share, while new companies raised funding to steal share and grow the market by targeting specific customer segments such as commuters. The average deal size doubled from $97.87 million to $252.65 million.

For the ride-sharing platforms, to expand or not is a question. According to Lyft, only 1% of the vehicle miles travelled (VMTs) in the US was made by ride-sharing platforms. This means a huge market to grow. However, expanding the existing market could also mean fewer resources allocated to autonomous driving: Uber exited several international markets and the autonomous truck market and tries hard to focus on autonomous cars, while Didi Chuxing tries hard to expand internationally and has been left behind in developing autonomous vehicles.

5. Scooter-sharing becomes a hype, but it will just stop there.

In 2017 and 2018, $595.73 million from 36 deals were invested into 21 scooter-sharing platforms. 7 companies received 79.56% of the total funding, and integration has already started. There will be little room for new entrants. On the other hand, given the low market barrier, the profitability of scooter-sharing business has long been questioned. Seeing the “failure” of the two largest bike-sharing platforms, investors may worry about the future of scooter-sharing platforms.

6. With a low entry barrier, the mobility-related service market is already saturated.

The total number and deals dropped half in this segment, while the total funding cut 57%. From information platforms for traffic, road, weather conditions to marketplaces for driver booking, parking services, and roadside assistance services, companies have been making finding information and services much easier than before. However, the market barrier is very low, the competition is intense, and the market is getting saturated in some domains. Investors only made 2 deals into the new companies, while they closed 21 deals in 2017. For the early-stage established companies, investors also cut their funding by half.

7. The vehicle service providers are growing and competing heavily.

This sector has attracted the fourth most substantial portion (14.57%, $17.76 billion) of total funding. Companies are improving traditional services (e.g. cleaning, maintenance, repair, dealership) by digitalizing (e.g. E-commerce for new cars and used cars) and using different models (e.g. O2O repair, mobile fuel-adding). Companies are also providing new services (e.g. vehicle charging service, connected car cloud, remote assistance, cybersecurity monitoring/protection platform, real-time vehicle condition monitoring) to cater the new needs of fleet owners and vehicle owners.

8. Automotive manufacturing is shrinking with limited innovation and a high volume of M&A activities.

In the auto parts manufacturing/distribution segment, 374 out of the 592 deals were M&A or buyout/LBO deals. In the automobile manufacturing segment, about half of the deals (85 deals) were closed by traditional non-EV manufacturers with 33 deals being M&A or buyout/LBO deals. Therefore, the average deal size was very high in automobile manufacturing ($318.95/$712.00 million in 2017/2018) and auto parts manufacturing ($315.50/$320.50 million in 2017/2018). Furthermore, most of the innovations in these two segments were not disruptive and would not bring dramatic changes to the industry.

Please find the full report here: https://blog.wen.fan/hello/mobility.

(Data spreadsheet: https://blog.wen.fan/hello/downloads/Automotive_Deals.xlsx.)